The USA's Housing Market: A Crisis Unfolding

There is a housing shortage in America, which many people feel but few are speaking about.

Amidst an unprecedented housing shortage, the aspirations of numerous potential homebuyers face daunting challenges. Regardless of generational affiliation, from hopeful Millennials to seasoned Baby Boomers seeking to downsize, the stark truth remains evident: there is a glaring inadequacy of available homes, with many lacking in quality or affordability for the average American. This housing crisis has persisted for three years, with indications pointing to another three to four years before substantial relief is in sight. A decade of affordable housing has been lost.

The Numbers

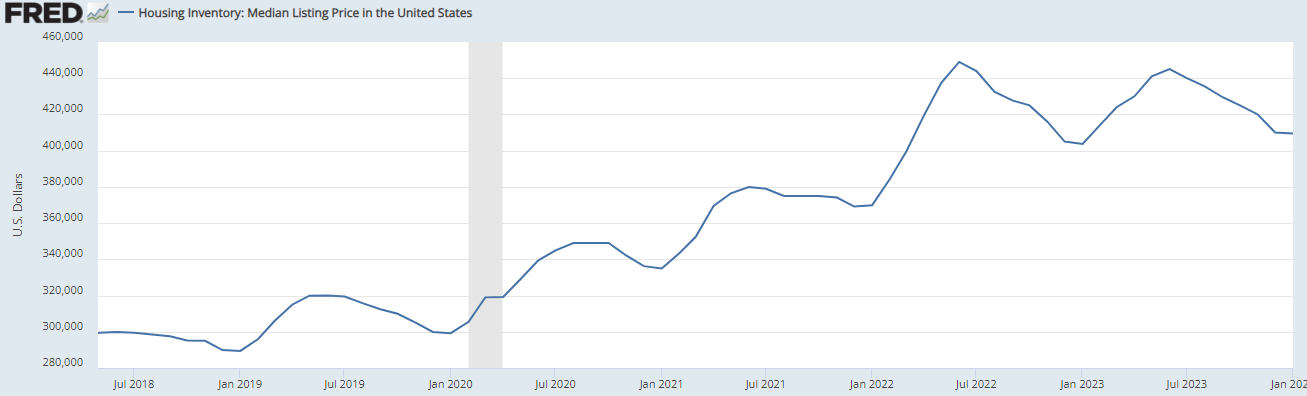

Skyrocketing Prices: The median listing price for homes in the United States has surged by a staggering 39% from June 2019 to June 2023. In just four years, we've witnessed a leap from $320,000 to $445,000 on average.

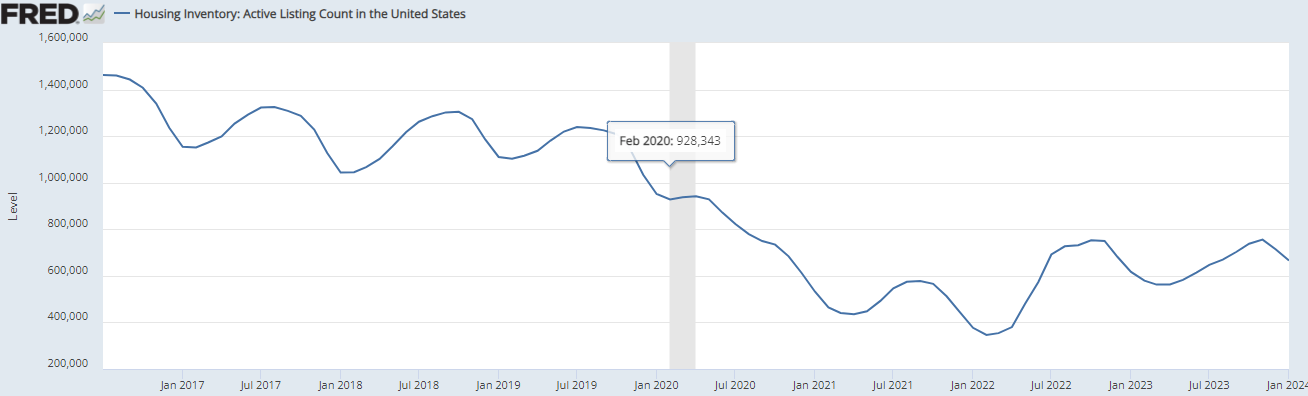

Dwindling Inventory: Since 2020, there's been a dramatic decline in the number of homes listed for sale. From July 2019 to January 2024, active listings in the United States plummeted by 39%. In July 2019, there were 1,239,534 homes listed, contrasting sharply with the mere 755,489 in January 2024. Typically, the housing market experiences a surge in listings during the summer months, with a decline in winter. However, there seems to be a slight uptick as of January 2024.

High Mortgage Rates: Mortgage rates have soared to their highest levels in almost 30 years, casting a shadow over the housing market. With borrowing costs reaching unprecedented heights, prospective homebuyers are facing significant hurdles in securing affordable financing. This surge in mortgage rates reflects a challenging landscape for those seeking to enter or navigate the housing market, marking a notable departure from the more favorable borrowing conditions seen in recent decades.

Affordability Crisis: According to a Redfin analysis of new listings in 97 major U.S. metropolitan areas, the number of affordable homes for sale has hit a record low. In 2023, there were only 352,500 affordable listings, marking a 40.9% decrease from the previous year's 596,135. This sharp decline is attributed partly to an overall drop in listings (down by 21.2% year over year) and partly to elevated mortgage rates and persistently high prices, making homes less attainable for many Americans.

The Story Behind the Numbers

In March 2020, the onset of the COVID-19 pandemic triggered mass panic, prompting federal and state governments to impose widespread lockdowns. These measures led to economic instability, causing businesses to fail and people being unable to work. In response, between February 2020 and April 2022 the Federal Government printed 43% more of new money into the economy bailing out corporations, extending unemployment benefits, and increasing spending.

The uncertainty surrounding the pandemic and lockdowns caused a significant reduction in home listings throughout 2020. As people hunkered down, fewer homes were put up for sale. This scarcity in housing supply contributed to the subsequent surge in prices. This uncertainty, caused by the economic instability of the lockdowns and fear of Covid-19, is certainly a major cause for the first major dip in housing listing.

Throughout 2021 and into 2022, prices in general started exploding from the continual injection of newly printed money. To combat the soaring prices (with CPI eventually peaking at 9%), the Federal Reserve increased the Federal Funds Rate. From March 2022 to August 2023, the Federal Reserve incrementally raised the Federal Funds Rate from .08 to 5.33. The increase was significant, because for the past two decades, the US has had a Federal Funds Rate of nearly zero. The interest rate was hiked up to 5.33%, aimed to address the inflationary pressures induced by the influx of new money into the economy during the lockdown period. As of January 2024, CPI is reported at 3.7%.

However, these higher interest rates have suppressed housing inventory. The higher the Federal Funds Rate, typically the higher the mortgage rates. The lower the Federal Funds Rate, typically the lower the mortgage rates. With mortgage rates essentially doubling from 3.5% to 5% in 2019 to 7% or 8% presently, potential sellers are disincentivized from listing their homes, fearing they'll be trading in a low-interest rate for a significantly higher one.

In essence, the response to lockdowns—printing money to support citizens—led to price inflation, prompting subsequent interest rate hikes. Now, prospective homeowners find themselves caught in a cycle of unaffordability and scarcity, with no easy way out.

As the housing crisis continues to unfold, it's evident that the road to recovery will be long and arduous. For now, Americans can only hope time might alleviate the strain and pave the way for a more accessible housing market.

A Lost Decade for Housing

As the Federal Reserve gears up for its upcoming meeting later this month, speculations abound regarding potential decreases in the Federal Funds Rate over the course of the year. The most recent Congressional Budget Office report suggest short-term interest rates will find a stable footing in the initial quarter of 2024, with a gradual descent expected until around mid-2027, followed by a period of stabilization. Projections indicate that the Federal Reserve will initiate a decrease in the federal funds rate, currently positioned between 5.25-5.50 percent, during the second quarter of 2024. This adjustment is attributed to a combination of decelerating inflation rates and escalating unemployment figures. By approximately mid-2027, analysts anticipate the federal funds rate to settle around 2.9 percent, maintaining a relatively consistent trajectory thereafter.

While such actions may, in the long run, translate into lower mortgage rates and a subsequent increase in housing inventory, the process of adjustment takes time. Consequently, if the Fed initiates interest rate cuts starting in March and continues throughout the year, we're poised to witness a sharp uptick in demand during the summer, coinciding with the traditional surge in seasonal demand. However, with inventory still lagging behind, prices are likely to rise far beyond what would be deemed reasonable.

In the immediate future, the outlook appears bleak, and the next few years won't offer much respite. Drawing insights from Mises' teachings, caution must guide our economic predictions. It's estimated that it will take three to four more years for the market to stabilize in response to the Federal Funds Rate reduction, paving the way for a semblance of normalcy to return. Naturally, certain regions may recover faster than others, but by the time the vast majority of areas regain equilibrium, nearly a decade of affordable housing opportunities will have slipped through our fingers.